The Hydrogen Boom: From Obscurity to Centre Stage (2020–2021)

Hydrogen emerged from decades of obscurity to become one of the defining clean-energy investment themes of 2020–2021. Global climate targets tightened, governments launched hydrogen strategies, and investors poured billions into electrolysers, fuel cells and hydrogen infrastructure.

The combination of ambitious climate policy, aggressive government funding, and strong corporate endorsements convinced investors that “the hydrogen economy” was imminent. The EU announced multibillion-euro hydrogen programs, the U.S. committed US$7 billion to hydrogen hubs and later added a US$3/kg production tax credit under the Inflation Reduction Act, and Australia and Canada rolled out their own multi-billion-dollar support frameworks. Companies like Plug Power, Ballard Power, Bloom Energy and Nel ASA surged as retail and institutional capital rushed into the sector. Fortescue Future Industries (FFI) added further legitimacy by committing to electrolyser manufacturing, hydrogen mobility and large-scale export ambitions.

Hydrogen had never been more in the spotlight.

Hydrogen Stocks Soared… Then Crashed Hard

As investor enthusiasm peaked, pure-play hydrogen stocks experienced some of the most dramatic price runs in the clean-tech universe — and then some of the most violent collapses.

Plug Power surged from under US$5 in 2019 to over US$60 in early 2021, fuelled by massive capital raises, aggressive growth targets and the expectation that hydrogen would become a mainstream industrial fuel within a few years. Ballard Power, FuelCell Energy, Bloom Energy, Nel ASA and other electrolysis and fuel-cell developers also reached multi-year highs. A new wave of hydrogen ETFs launched and retail investors piled in, convinced they were buying into the next major clean-energy revolution.

It didn’t last. As costs remained high, offtake struggled to materialise and policy clarity lagged, the market violently repriced the entire sector. Plug Power collapsed more than 95%, returning to around US$1 by mid-2025. Ballard Power and FuelCell Energy fell more than 60–85% from their peaks. Nel ASA, Green Hydrogen Systems and several smaller electrolyser players saw similar declines. Billions in market value evaporated, and hydrogen fell out of favour almost overnight.

Hydrogen stocks became a case study in how quickly hype cycles can reverse.

Chart: The rise and fall of a hydrogen stock. Example – Plug Power (PLUG) share price spiked from under $5 to over $60 during the 2020-2021 hydrogen boom, then collapsed back to nearly $1 by mid-2025. Hydrogen investors faced a wild ride as hype gave way to harsh realities.

The Crash: Reality Catches Up (2022–2024)

The reversal was driven by a combination of economic, technical and policy factors. Green hydrogen remained expensive at US$5–10/kg, well above fossil-derived hydrogen. Electrolyser scaling was slower and more costly than expected. More importantly, most announced projects lacked committed buyers — a fatal flaw for infrastructure that requires long-term revenue certainty.

By late 2024, only a small percentage of global hydrogen projects had reached final investment decision. Several high-profile developments were cancelled outright across Europe, North America and Asia, including blue and green hydrogen projects from Shell, Equinor, Repsol and Air Products. At the same time, interest rates spiked, making capital-intensive hydrogen plants even harder to finance.

Policy delays further undermined confidence. The U.S. Treasury took nearly two years to publish rules governing IRA hydrogen subsidies, freezing investment. The EU’s complex renewable hydrogen certification requirements caused project uncertainty. With no clear offtake, no stable policy and rising costs, the market turned sharply.

The hype cycle had crashed into reality.

Hydrogen Fell Out of the Headlines — But Not Out of the Future

Despite the dramatic correction, hydrogen remains essential to global climate strategies. Heavy industries such as steel, ammonia, chemicals, shipping and long-haul mobility require hydrogen-based solutions — sectors where batteries cannot provide the energy density or industrial heat required.

While headlines faded, committed investment continued. As of 2025, more than US$110 billion in clean hydrogen projects have reached FID globally. Over 1,700 hydrogen projects have been announced since 2020, with more than 500 now progressing meaningfully. Instead of 1–2 GW mega-projects, the sector has shifted to 10–100 MW electrolysers tied to ammonia plants, hydrogen hubs, industrial clusters and transport pilots. These smaller but commercially grounded deployments have real customers and viable economics.

Governments are also shifting from “announce funding” to “create demand.” Europe has implemented hydrogen usage mandates for industry, Japan and Korea are signing long-term ammonia import contracts, the U.S. hydrogen hubs are beginning to anchor regional clustering, and Australia is building out Hydrogen Headstart alongside emerging offtake mechanisms.

Hydrogen is no longer a hype-driven story — it’s a slow, essential industrial transition.

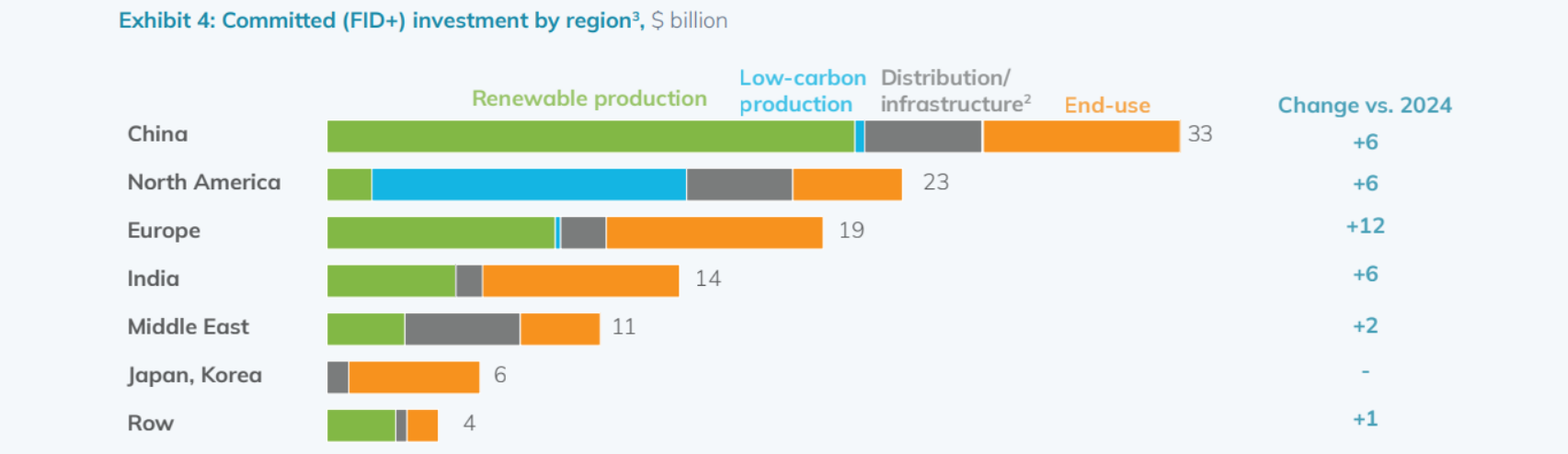

Figure 2. Committed Clean Hydrogen Investment by Region (FID+, 2025)Global committed hydrogen investment now exceeds US$110 billion. China leads with US$33B, followed by North America (US$23B) and Europe (US$19B). Australia and the Middle East account for most of the remaining ~US$35B.

Australia, North America and a More Credible Hydrogen Sector

Australia remains one of the world’s strongest long-term hydrogen candidates due to its renewable resource base. ENGIE/Yara’s Yuri project is supplying green hydrogen for ammonia production, Fortescue’s Queensland electrolyser factory is coming online, and mobility pilots in mining are expanding rapidly. Rather than betting on giant export-only projects, Australia is now focused on hydrogen hubs, ammonia export pilots and decarbonising domestic industry.

North America continues to benefit from the IRA’s production tax credits and regional hydrogen hubs. Canada’s Alberta and BC regions remain global leaders in blue hydrogen and fuel cell technology. The U.S. is advancing hydrogen storage, mobility and industrial clusters despite political volatility.

Globally, the sector is finally moving from vision to execution. The unrealistic mega-projects have largely dropped away, leaving a more investable landscape of practical, industrial deployments with real customers.

Key Hydrogen Stocks to Watch

Australia

- Fortescue (ASX: FMG) — Integrated green hydrogen strategy; electrolyser manufacturing; global export ambitions.

- Pure Hydrogen (ASX: PH2) — Hydrogen mobility and distributed production.

- Hazer Group (ASX: HZR) — Turquoise hydrogen via methane pyrolysis.

United States

- Plug Power (NASDAQ: PLUG) — Vertically integrated hydrogen ecosystem; extreme volatility; potential turnaround.

- Bloom Energy (NYSE: BE) — Solid oxide electrolysers + stationary power systems.

- FuelCell Energy (NASDAQ: FCEL) — Carbon capture + industrial power plants.

Canada

- Ballard Power (TSX/NASDAQ: BLDP) — Global heavy-transport fuel cell leader.

- Air Products (NYSE: APD) — Industrial gas major; world-scale hydrogen and ammonia developments.

The Next 5–10 Years: A More Investable Phase Ahead

The hydrogen sector is entering a mature, disciplined era. Costs continue to fall, technology is improving, and governments are shifting from broad funding announcements to targeted demand creation. Industrial offtake — the missing ingredient of the 2020–2021 boom — is beginning to crystallise.

Valuations are now significantly lower and business models far clearer than during the hype years. Hydrogen will not dominate the global energy system overnight, but it will become indispensable for heavy industry, shipping and long-duration storage.

Hydrogen isn’t dead — it’s maturing. And for long-term investors, that may be the most compelling phase of all.