📊 We initiated coverage on this one. In March, Cashu Research initiated coverage on Victory Metals with a Buy rating and an A$3.50 price target… against a share price of around A$1.40 at the time of the report. The full initiation report covers our valuation, the key catalysts, and the risk factors in detail. What follows is the story behind that call.

The defining market story of 2026 is a wall of liquidity chasing AI. Marquee tech IPOs and a handful of mega-caps are soaking up an extraordinary share of the world's investable capital. The S&P 100 has rarely been this top-heavy.

Here's the asymmetric risk almost nobody is pricing: China is sitting on far cheaper AI models that could be just as good. If they drop those into the market at scale, the entire premium being paid for Western AI exceptionalism gets called into question overnight.

And when a market that concentrated unwinds, the liquidity doesn't evaporate. It hunts. It chases the things that actually matter in a de-globalising world: critical metals and heavy rare earths.

Victory Metals (ASX: VTM) is being built right in front of that wave.

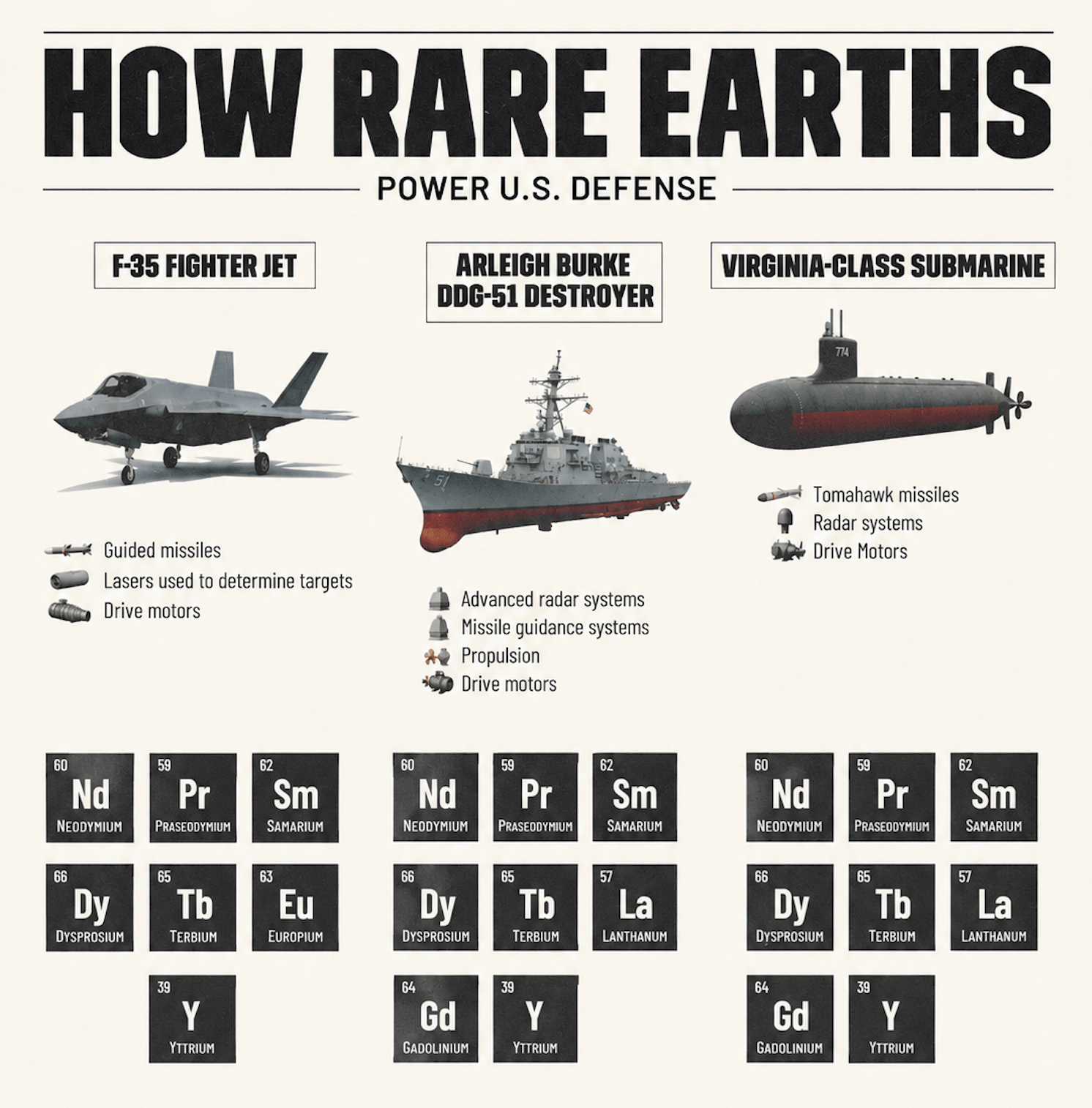

The 90% chokehold

The irony at the heart of the rare earth story is this: China controls roughly 90% of the global heavy rare earth supply chain. These minerals aren't a bargaining chip in the trade war…..they are the leverage.

Terbium, yttrium and dysprosium power F-35 fighter jets, Virginia-class submarines, missile guidance systems and offshore wind turbines. There is no substituting them, and today there is almost no way to source them outside China.

That's why every Western government now treats secure, non-Chinese heavy rare earth supply as defence infrastructure, not a commodity bet. The market is already pricing structural shortage in these elements and no AI headline, in either direction, fixes that supply gap.

The same metals are inside the AI boom itself

Here's the part that makes the rotation thesis even cleaner: heavy rare earths aren't just defence metals. They're wired into the AI buildout too.

Terbium and dysprosium are used in semiconductors and the high-performance magnets that fill data centres - in the cooling systems, drives and power infrastructure that keep compute running. Yttrium goes into the high-temperature superconductors and laser systems behind chip manufacturing. The same elements the Pentagon can't substitute are sitting inside the AI supply chain.

That's the asymmetry. If the AI premium gets called into question, the companies trading at perfection-priced multiples get repriced but the compute demand doesn't vanish. AI is here to stay; not every company will make the cut. When that shakeout comes, the smart money stops paying any price for the story and starts valuing the scarce inputs keeping the industry afloat. The picks and shovels get re-rated while the crowded trade deflates.

Either way the AI story breaks, the metals win. That's the position VTM occupies.

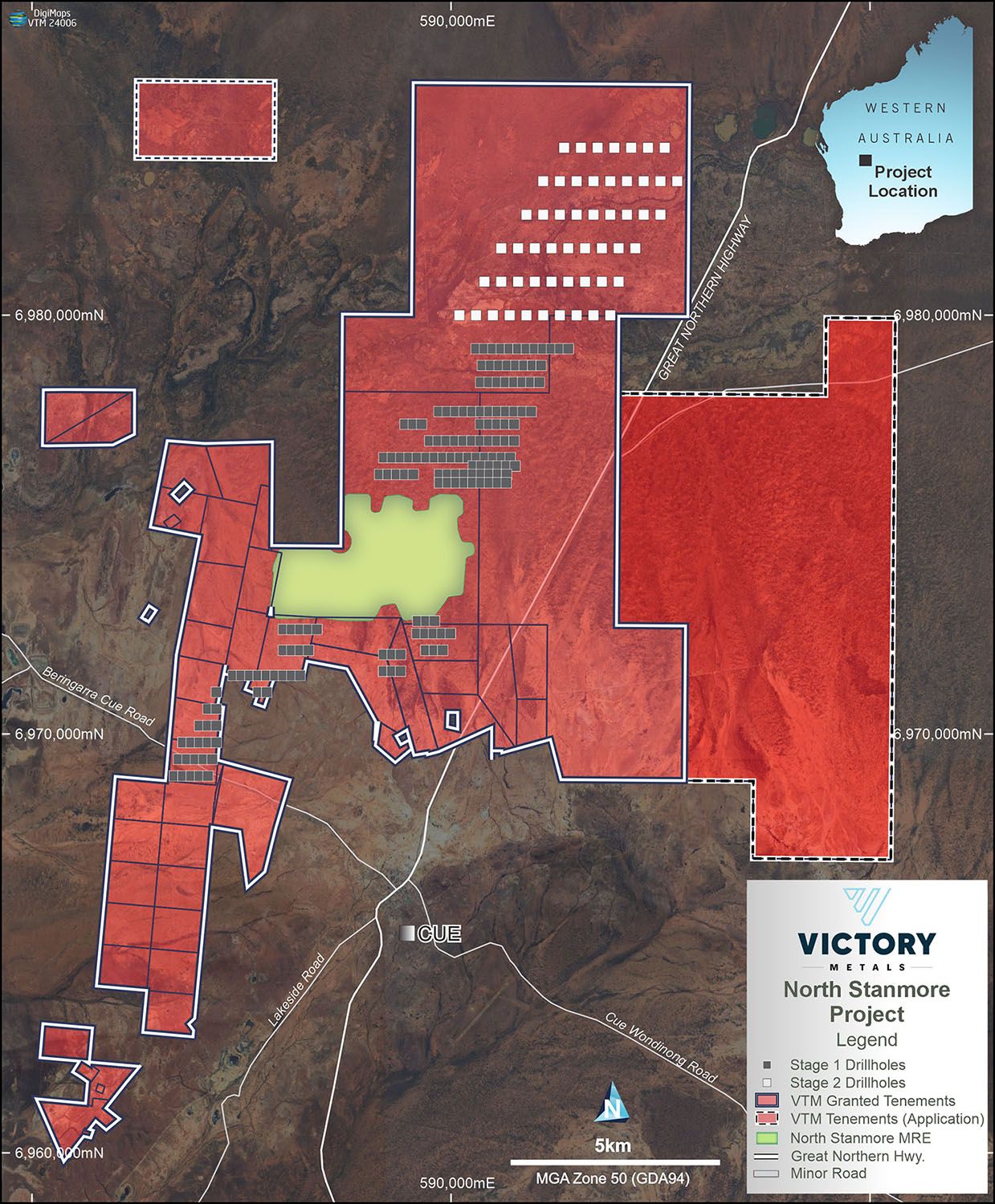

Australia's largest heavy rare earth clay project

Victory's North Stanmore project, near Cue in Western Australia, is Australia's largest and most advanced heavy rare earth clay project, with a 321 million tonne JORC-compliant resource supporting a mine life of more than 60 years.

It is one of the only non-Chinese sources proven to produce all seven of the restricted heavy rare earth elements including terbium, yttrium and dysprosium.

The heavy-to-total rare earth ratio averages 39% and reaches up to 83% in the best zones - one of the most premium heavy rare earth profiles anywhere in the world. The deposit sits on 100% Crown land in a Tier-1, mining-friendly jurisdiction with no landowner disputes and no resettlement risk, adjacent to road, rail, airport and port infrastructure.

North Stanmore tenement map — source: victorymetalsaustralia.com

The scoping study numbers: an NPV of A$1.2 billion, a 52% IRR, operating costs of just A$25.50 per ROM tonne, and a targeted 2-year capital payback.

This isn't blowing-up-mountains mining

Most people think rare earth mining means deep extraction, blasting, and energy-hungry processing circuits. North Stanmore is a fundamentally different beast, because the deposit sits near-surface in clay.

That changes the entire economics. Shallow open-cut extraction with no blasting. Simple, low-cost physical beneficiation instead of complex crushing circuits. And leach kinetics that border on absurd: roughly 80% of the rare earths are recovered within just 30 minutes, where industry-standard assumptions run hours to days.

Lower capex, faster processing, quicker path to market. In a race to fill the Western supply gap, that timing advantage is everything. Victory is targeting commissioning in Q3 2028, positioning North Stanmore as one of the first new Western heavy rare earth projects to reach production this decade.

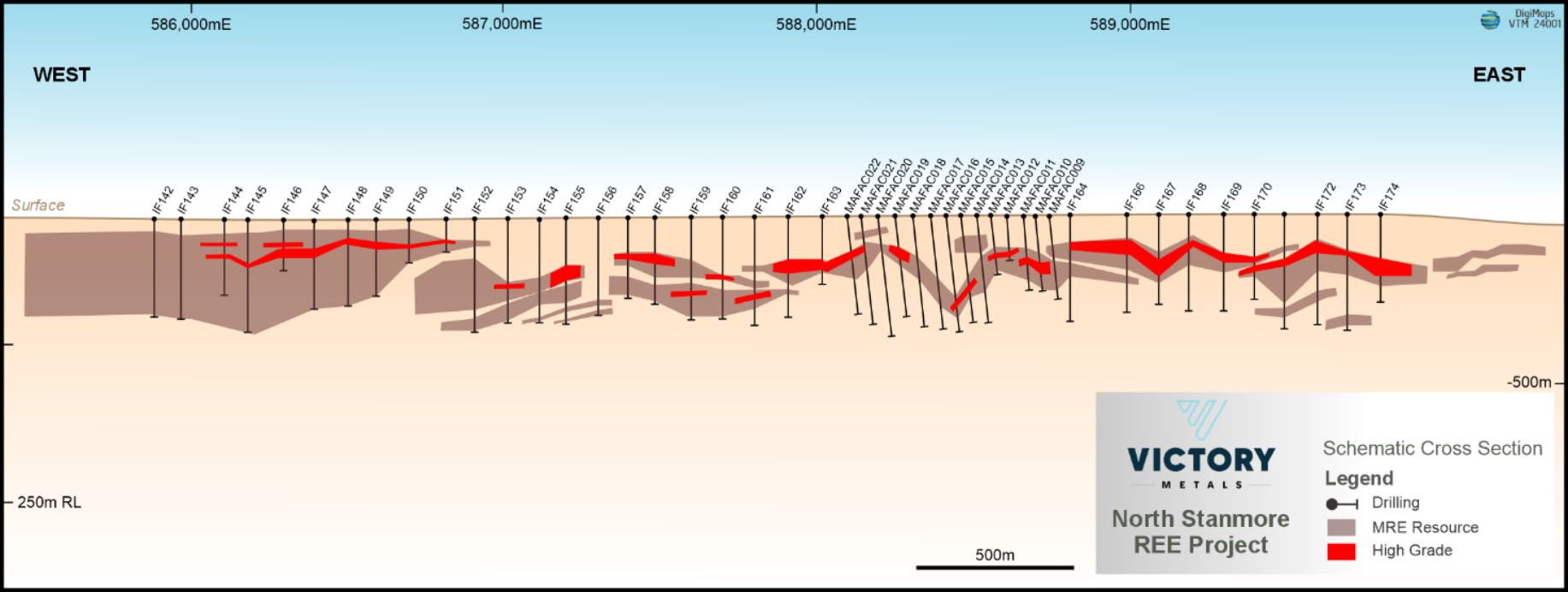

The breakthroughs keep coming

In March 2025, first-pass flotation test work delivered a 48x upgrade in rare earth concentration - from raw ore to 5.9% total rare earth oxide - confirming the potential for a simple, low-cost beneficiation circuit.

Critically, the premium wasn't diluted: even after concentration, the deposit held its 38% heavy-to-total ratio. The high-value heavy rare earth profile survives processing intact.

Drill results — source: victorymetalsaustralia.com

Washington has already noticed

This is not a speculative story waiting for its first customer.

The US EXIM Bank has issued a Letter of Interest for up to US$190 million in potential financing direct US government-backed recognition of North Stanmore's strategic value. Victory has also signed a non-binding LOI with Summit OMO Corporation, signalling offtake and partnership interest from a credible buyer.

A genuine re-rating is underway as rare earth fundamentals strengthen and Western supply-security urgency builds.

What's next

Q2 2026: the Pre-Feasibility Study - the next major de-risking event, with PFS-level CAPEX definition set to sharpen the investment case significantly.

Through 2026–2027: project financing and strategic partnership finalisation.

Q3 2028: targeted commissioning.

The PFS is imminent.

The bottom line

Victory Metals (ASX: VTM) sits at the intersection of the two biggest structural forces in markets right now: a dangerously top-heavy AI trade, and a Western world scrambling to break China's 90% grip on the heavy rare earths that power its defence hardware.

North Stanmore is Australia's largest heavy rare earth clay project - 321 million tonnes, 60+ years of mine life, all seven restricted heavy rare earths, a A$1.2 billion NPV scoping study, and a US$190 million EXIM Letter of Interest behind it. The clay geology means it can move faster and cheaper than almost any hard-rock competitor, with commissioning targeted for Q3 2028.

That's the disconnect our research team flagged when Cashu Research initiated coverage with a Buy rating and an A$3.50 price target: the market is still valuing VTM like a typical early-stage developer, while the underlying project is increasingly being treated as a strategic asset.

Rare earth prices are volatile, and development-stage mining carries real risk…this is still a project being built, not a producer. But whatever happens to the AI trade, the strategic-minerals problem only gets more urgent. When the rotation comes, the capital will go looking for scarce, strategic, hard assets that the West actually needs.

The ticker is VTM on the ASX

Disclaimer: This content has been produced on behalf of Victory Metals Limited (ASX: VTM). This newsletter is for informational purposes only and is not financial advice. It is part of a paid marketing campaign. The Buy rating and A$3.50 price target referenced are from the Cashu Research initiation report dated 17 March 2026 and reflect the analyst's opinion at that date; price targets are not guarantees of future performance and may not be achieved. Cashu Group, its directors, employees or associates may hold or trade securities in Victory Metals. Cashu Group was compensated by Victory Metals Limited for the creation and distribution of this content. Always conduct your own research before making any investment decision. Past performance is not indicative of future results. Investing in development-stage mining companies carries significant risk, including the potential loss of capital. Macro commentary regarding AI-related equity concentration is structural commentary, not a dated market prediction. All project figures referenced come from the Victory Metals scoping study and company public disclosures. Always do your own due diligence and consult a licensed financial professional before making investment decisions.